The cooking oil market in Vietnam has seen tremendous growth in recent years and is poised to continue its upward trajectory. Driven by a fast-growing population, rising incomes, and changes in dietary habits, demand for cooking oils of all types has surged. Both local producers and international companies see significant opportunities in this rapidly expanding sector. However, players in the Vietnamese cooking oil market also face fierce competition from various brands both local and international. With the right marketing strategies, brands can stand out to benefit for years from this market.

I. A RISING DEMAND FOR COOKING OIL

Despite the well-established status of the cooking oil industry in Vietnam, there are still ample opportunities for new entrants. Presently, the consumption of cooking oil among the Vietnamese population falls below the WHO-recommended standard of 13.5kg/year. Nevertheless, it is projected that in the near future, this figure will rise to approximately 16.2 – 17.4 kg/person/year, and by 2025, it is expected to reach 18.6 – 19.9 kg/person/year.

The growing population is driving up demand for food and household goods, including cooking oils. Furthermore, Vietnam’s economy is expanding at an average of 6-7% annually, more citizens are entering the middle class. This has increased their disposable income and spending power, including on higher quality cooking oils.

As lifestyles become busier and more urbanized, Vietnamese consumers are eating out more and consuming more convenience and fast foods that are deep-fried or cooked with oil. This is increasing the amount of cooking oil used. Besides, the booming restaurant industry and growth of food delivery apps have also raised the demand for bulk cooking oils among commercial food preparation establishments.

According to market research firm Nielsen, the size of the cooking oil market in Vietnam is estimated at 30,000 billion VND/year and continues to grow each year. This has attracted a lot of investment from domestic and foreign enterprises.

II. MOST POPULAR TYPES OF COOKING OIL

1) Palm Oil

Palm oil dominates the Vietnamese cooking oil market, holding over 50% of the total volume share. It has been the preferred choice of both commercial and home kitchens for decades due to its many advantages.

Palm oil is easily available from local and imported sources at stable prices. It is generally the most affordable cooking oil option, which is important for price-sensitive Vietnamese consumers. The relatively inexpensive palm fruit can also be processed into oil using traditional methods, making it accessible even in rural areas.

The mildly flavored and neutral-colored palm oil is suitable for a wide range of Vietnamese dishes. It is the oil of choice for stir-frying noodles, steaming dumplings, and shallow frying of various meats and seafood. Commercial establishments rely heavily on palm oil for its stability, high smoking point, and ability to withstand repeat usage.

2) Soybean Oil

Soybean oil, produced domestically from locally grown soybeans, is the second most commonly used cooking oil in Vietnam after palm oil. It accounts for around 30-35% of the total cooking oil market by volume.

Soybean oil has several attributes that appeal to Vietnamese consumers. It has a distinct but light taste that some prefer over flavorless palm oil. The lighter taste also makes soybean oil suitable for a wider range of dishes, including dipping sauces, marinades, and salad dressings in addition to stir frying and deep frying.

Compared to imported oils, soybean oil is more affordable and accessible for many Vietnamese people, especially in rural areas where soybean cultivation is prevalent. Domestic production also contributes to Vietnam’s food self-sufficiency and security goals.

From a health perspective, soybean oil contains lower saturated fat and more polyunsaturated and monounsaturated fatty acids than palm oil. This has led some health-conscious consumers to switch from palm oil to soybean oil, believing it is a “healthier” option.

3) Canola Oil

Canola oil, produced from rapeseed that has been genetically modified to reduce certain toxic compounds, has seen increasing popularity in Vietnam in recent years. However, it still accounts for a relatively small market share of around 5-10% compared to dominant oils like palm and soybean.

Canola oil appeals to health-conscious Vietnamese consumers due to its claimed nutritional profile. It contains a lower proportion of saturated fat and a higher amount of monounsaturated fatty acids compared to other common vegetable oils. This has led many consumers to perceive canola oil as a “healthier” choice.

However, canola oil’s higher price point limits its consumption mostly to upper and upper-middle-income households in Vietnam. At around 1.5 to 2 times the cost of palm oil, canola oil remains an aspirational purchase for many consumers. Its more limited availability from both imported and domestic sources is also a constraining factor.

4) Sunflower Oil

Sunflower oil accounts for a tiny share – likely under 5% – of Vietnam’s cooking oil market, making it a niche product. Sunflower oil is mostly imported and consequently has a higher price tag compared to dominant local oils like palm and soybean.

However, sunflower oil is gaining some ground in Vietnam due to its perceived health and nutritional benefits. High-oleic sunflower oil varieties that are higher in monounsaturated fatty acids and lower in saturated fats have been marketed as a “healthier” option for cooking. However limited availability and considerably higher prices continue to constrain sunflower oil’s penetration in Vietnam. At around 2 to 3 times the cost of palm oil, sunflower oil remains out of reach for mainstream consumers. It mostly targets health-conscious and affluent households.

5) Vegetable & Fish Oil Blends

Vegetable and fish oil blends remain a tiny niche in Vietnam’s cooking oil market, likely accounting for less than 1% of the total volume. These blended oils combine various vegetable oils like canola, sunflower, or soybean with marine or fish oils.

Blends containing Omega-3 fatty acids from fish oil are marketed as providing certain health benefits like supporting heart, brain and eye health. They are positioned as “functional” or “nutritive” oils rather than purely for cooking purposes.

However, these blended oils face several constraining factors that limit their appeal and penetration in Vietnam. Their higher costs, often 2 to 3 times that of mainstream oils, restrict consumption mostly to high-income households.

III. FIERCE COMPETITION

The Vietnamese cooking oil market is currently facing intense competition due to the entry of foreign cooking oil brands.

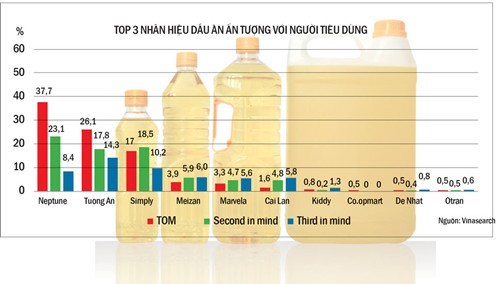

According to statistics from the Ministry of Industry and Trade, there are around 40 companies involved in the production and trading of cooking oil in Vietnam. Among these, palm oil constitutes 70 percent of the market, while soybean oil accounts for 23 percent.

A major domestic player in the cooking oil industry, Kinh Do Corporation (KIDO), reported a decline in its cooking oil revenue during the second quarter. The corporation’s earnings dropped by more than 20 percent, totaling 1.67 trillion VND (approximately 72.2 million USD). Among KIDO’s three-member companies operating in the cooking oil segment, only Golden Hope Nha Be Edible Oils Co., Ltd managed to maintain profitability from April to June.

During the same period, Tuong An Vegetable Oil Company (TAC) recorded 869 billion VND in revenue, witnessing a year-on-year decrease of 14 percent, while Vietnam Vegetable Oils Industry Corporation (Vocarimex) experienced a significant drop of 35.21 percent, reaching 694 billion VND in revenue.

Despite the formidable challenges and strong competition, KIDO still perceives the cooking oil sector as an attractive industry, given its vast market and potential purchasing power.

In 2014, Sao Mai Group, known for its focus on property trading and seafood processing, ventured into the cooking oil market by introducing its premium fish oil brand, Ranee. Despite the competitive nature of the market, the company remains resolute in its decision, as there are currently no domestic or foreign producers manufacturing cooking oil from tra fish.

Additionally, the logistics services provider, Daso Group, recently launched two new vegetable oil brands named Ogold and Binh An. Meanwhile, Quang Minh Vegetable Oil Joint Stock Company produces cooking oil under the brands Mr. Bean, Soon Soon, and Oilla.

The current consumption of cooking oil in Vietnam is estimated at 9.5 kilograms per person per year, falling below the World Health Organisation’s (WHO) recommended level of 13.5 kilograms. Consequently, the business community sees great potential and opportunities in the Vietnamese cooking oil market.

IV. HEAVILY DEPENDENT ON IMPORTS

Vietnamese manufacturers can only fulfill approximately 40 percent of the total demand for cooking oil, which amounts to approximately 1.5 million tonnes annually. Consequently, the country relies heavily on imports, including significant quantities from Malaysia.

During the first half of the year, Vietnam imported 242,700 tonnes of cooking oil from Malaysia, which is 23,200 tonnes more than in the same period in 2018. The promising prospects in the Vietnamese market have prompted several Malaysian companies to consider investing or expanding their operations in this Southeast Asian country.

Over the past few years, foreign enterprises like Musim Mas Group (Singapore), one of the world’s largest vegetable oil producers, have established cooking oil factories in Vietnam, with an investment of 71.5 million USD and a designed capacity of 1,500 tons per day. Through their distribution company, ICOF Vietnam, Musim Mas has introduced high-quality cooking oils to the Vietnamese market. The company has great confidence in the brand’s development in Vietnam, given the increasing interest of Vietnamese consumers in healthy products.

IV. SUMMARY

In conclusion, cooking oil is undoubtedly a hot market in Vietnam today. Rising demand coupled with opportunities for both importers and local producers points to continued growth potential. However, challenges around price fluctuations, competition, and product quality must also be navigated. Government policies aimed at supporting local industries while maintaining food safety and quality standards will play a role in shaping the market. As Vietnamese consumers’ incomes and preferences continue to evolve, the cooking oil sector will adapt to meet changing demands. If able to provide high-quality, affordable products and brands that meet consumers’ needs, companies operating in Vietnam’s cooking oil market are poised for success in the years ahead.

Searching for a local agency to promote your brands in Vietnam? Contact us!